The Bitcoin “What If” Scenario Every Advisor Should See

Modernizing the 60/40 Portfolio – With Just a Touch of Bitcoin

The Crypto Advisor is your trusted resource for navigating the world of cryptocurrency. Each week, we deliver a clear and concise update on the latest developments in crypto, straight to your inbox. This is more than just a newsletter; it’s an essential resource for forward-thinking advisors focused on maintaining a competitive edge. We’re excited to support your journey in adapting to and thriving in the new age of financial services.

The Bitcoin “What If” Scenario Every Advisor Should See

New research from Bitwise shows that even a small allocation to Bitcoin has historically improved returns, boosted Sharpe ratios, and modernized traditional portfolios – all with surprisingly modest increases in risk.

For more than 50 years, the 60/40 portfolio (60% equities, 40% bonds) has been the foundation of modern asset allocation. But with structural shifts in markets, persistent inflation concerns, and a new generation of investors, many advisors are asking: is it time to rethink the core?

Back in April, Bitwise released an updated version of its flagship white paper, Bitcoin’s Role in a Traditional Portfolio. The findings make a compelling case that Bitcoin – long viewed as speculative – may now serve as a meaningful portfolio enhancer.

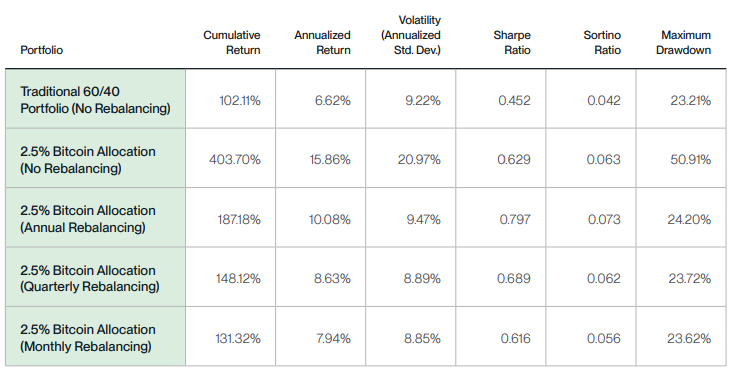

A Decade of Data, No Cherry-Picking

The Bitwise team didn’t rely on anecdotes or handpicked timeframes. Instead, they analyzed every one-, two-, and three-year rolling period from January 2014 through December 2024, testing allocation sizes from 0% to 10% and multiple rebalancing strategies.

The base portfolio used in the study reflects what many advisors already implement:

– 60% Vanguard Total World Stock ETF (VT)

– 40% Vanguard Total Bond Market ETF (BND)

Only Bitcoin’s price returns were used – no hard forks, airdrops, or artificial boosts.

Headline Results with Just 2.5% Bitcoin

With quarterly rebalancing and a 2.5% allocation to Bitcoin:

– Returns improved in 74% of one-year periods

– 93% of two-year periods

– 100% of three-year periods

On a median three-year basis, that 2.5% allocation added 11 percentage points to cumulative returns – without materially increasing volatility or max drawdowns.

Most notable: the Sharpe ratio improved by 51%, signaling a major boost in risk-adjusted performance.

“When considering these investing parameters on a historical basis, it is hard to overstate the power and consistency of bitcoin as an enhancer of diversified portfolios.”

– Bitwise White Paper

Three Key Questions for Advisors

The white paper addresses the core concerns most advisors face when evaluating a Bitcoin allocation:

1. What’s the minimum acceptable holding period?

Longer holding periods produced more consistent results:

– Positive contribution in 74% of one-year periods

– 93% of two-year periods

– 100% of three-year periods

Even in the worst one-year window, Bitcoin reduced returns by less than 3 percentage points. In the best, it added over 16.

Bottom line: Bitcoin rewards patience. Advisors should take a multi-year view.

2. What’s the best rebalancing strategy?

Rebalancing is essential with volatile, asymmetric assets like Bitcoin. Bitwise compared multiple rebalancing approaches, but found that quarterly rebalancing provided a strong balance between capturing upside and managing risk.

3. How Much Bitcoin Should You Add?

The sweet spot, historically, lies between 2% and 5%.

Cumulative returns rise almost linearly as you add more Bitcoin

Sharpe ratios plateau around the 5% allocation

Max drawdowns remain modest up to around 4.5% Bitcoin, but spike beyond that

In other words, small allocations can make a big difference. Going all-in isn't necessary or wise for most portfolios.

Addressing Volatility Concerns

Bitcoin’s reputation for volatility is well-earned, but that volatility isn’t always a liability - particularly when it's uncorrelated to traditional asset classes.

Over the full study period:

Bitcoin rose from $755 to over $93,000

Despite multiple 50%+ drawdowns, its low correlation with stocks and bonds provided diversification benefits

This means Bitcoin’s short-term volatility may actually dampen overall portfolio swings when added in small doses, thanks to the classic power of diversification.

Behavioral Implications for Clients

Bitwise wisely notes that investor psychology matters. While a 10% Bitcoin allocation would have delivered the highest cumulative return, it also carried drawdowns north of 29% - a level that may be emotionally intolerable for some clients.

At 2.5% to 5% allocations, drawdowns remain close to those of the base 60/40 portfolio while adding significant upside potential. Advisors can use this to craft conversations around:

Client risk tolerance and time horizon

The asymmetric nature of Bitcoin’s return profile

The role of non-correlated assets in modern portfolios

Practical Takeaways for Advisors

If you're a financial advisor navigating digital assets, here’s what this study means in plain terms:

Bitcoin has graduated from speculative sideshow to portfolio enhancer

Modest allocations (2% to 5%) can boost returns without derailing risk profiles

Quarterly rebalancing offers a practical path to control volatility

Three-year-plus time horizons are key to maximizing benefit and minimizing regret

Whether you’re crypto-curious or already crypto-confident, the data here is a compelling tool for conversations with clients and for your own allocation strategies.

A Tip of the Hat to Bitwise

Kudos to the team at Bitwise – Matt Hougan, Gayatri Choudhury, and Mallika Kolar – for producing such a rigorous and balanced study. As always, their research leads the industry in clarity, depth, and actionable insight.

You can download the full white paper here: Bitcoin’s Role in a Traditional Portfolio – Bitwise Investments

Bank of America Is Developing A Stablecoin - Here’s What RIAs Should Know

Crypto doesn’t necessarily need another stablecoin – but that hasn’t stopped Bank of America from trying to build one.

In a recent interview, CEO Brian Moynihan confirmed that the bank is actively developing a fully dollar-backed stablecoin. The project remains in its early stages: no public name, no timeline, and no clearly defined use case. Still, Moynihan was direct – launching a stablecoin is no longer optional if the bank wants to remain competitive. There’s even been speculation about a possible partnership with JPMorgan, though nothing has been confirmed.

At a high level, this move is significant. One of the largest U.S. banks entering the stablecoin space marks a clear legitimization of the asset class – particularly for institutional investors still on the sidelines. But legitimacy doesn’t always mean innovation. Just last week, The Wall Street Journal reported that Amazon is teaming up with Walmart to explore launching a stablecoin.

Looking ahead, it’s hard to imagine a future with dozens of stablecoins operating at scale. Consolidation seems far more likely, with incumbents like Tether (USDT) and Circle (USDC) continuing to dominate. In that context, Bank of America’s stablecoin feels less like a breakthrough and more like a “me-too” product – especially in the absence of a compelling value proposition.

Unless BofA can deliver something materially different – better interoperability, lower friction, or broader utility – its stablecoin may be destined for redundancy or eventual acquisition.

One more development to watch: President Donald Trump recently endorsed the GENIUS Act, legislation designed to support stablecoin innovation and ensure dollar-backed stablecoins are issued within the U.S. regulatory perimeter. Between Bank of America’s ambitions and Trump’s policy pivot, stablecoins are no longer just a crypto topic – they’re entering both boardrooms and campaign platforms.

The SEC Hosted A Roundtable On Decentralized Finance

At the SEC’s recent “DeFi and the American Spirit” roundtable, Commissioner Hester Peirce made a strong case that decentralized finance aligns with foundational American principles – including private property rights, economic liberty, and open innovation.

Peirce described blockchains as transformative tools for enabling peer-to-peer ownership and exchange without centralized intermediaries. She underscored the importance of preserving self-custody through digital wallets and welcomed recent staff clarification that network participants – such as validators and staking providers – are not automatically engaged in securities transactions. Still, she emphasized that formal rulemaking is needed, not just interpretive guidance.

Peirce was critical of the prior administration’s regulatory approach, arguing that unclear policies and enforcement-driven tactics stifled innovation. Developers, she noted, should not be treated as brokers for merely writing code. She called for an update to outdated securities laws to account for self-executing, on-chain software.

To responsibly support crypto innovation, Peirce proposed a new “innovation exemption” – a framework that would allow compliant blockchain projects to launch under clearly defined conditions. She positioned these reforms as essential for maintaining U.S. leadership in digital asset innovation, echoing recent calls by former President Trump to make the U.S. the “crypto capital of the planet.”

For advisors, this signals growing political and regulatory momentum behind DeFi – and an increasing likelihood that policy frameworks may shift in ways that affect portfolio strategy, custody, and client engagement.

From Crisis to Code: How Bitcoin Was Born

Bitcoin was born out of the 2008 financial crisis, when a pseudonymous figure named Satoshi Nakamoto proposed a new concept: a decentralized, peer-to-peer currency that didn’t require banks or governments to validate transactions. The innovation that made it possible was blockchain – a tamper-resistant, shared ledger that records transactions transparently, without intermediaries.

The first block, known as the “genesis block,” was mined in January 2009. With it, Bitcoin officially launched – and a new era in digital finance began.

Earlier attempts at digital money, such as DigiCash and B-Money, had failed primarily because they relied on centralized systems to verify transactions – making them vulnerable to control, censorship, and systemic risk. Blockchain solved that problem by distributing verification across a global network, dramatically improving both transparency and security.

For RIAs, understanding Bitcoin’s origin story is more than historical context – it’s key to understanding the asset’s core purpose. Bitcoin isn’t just a speculative trade – it’s a breakthrough in how value can be stored, transferred, and secured in a digital world.

Disclaimer: The information provided by The Crypto Advisor is for educational and informational purposes only and does not constitute financial, investment, or legal advice. The Crypto Advisor is not a registered investment advisor, broker-dealer, or financial planner. Nothing in this email should be interpreted as a recommendation to buy, sell, or hold any financial instrument or investment. Always consult with a licensed financial professional before making any investment decisions.